Clean Energy Venture Capital, Why We Invested

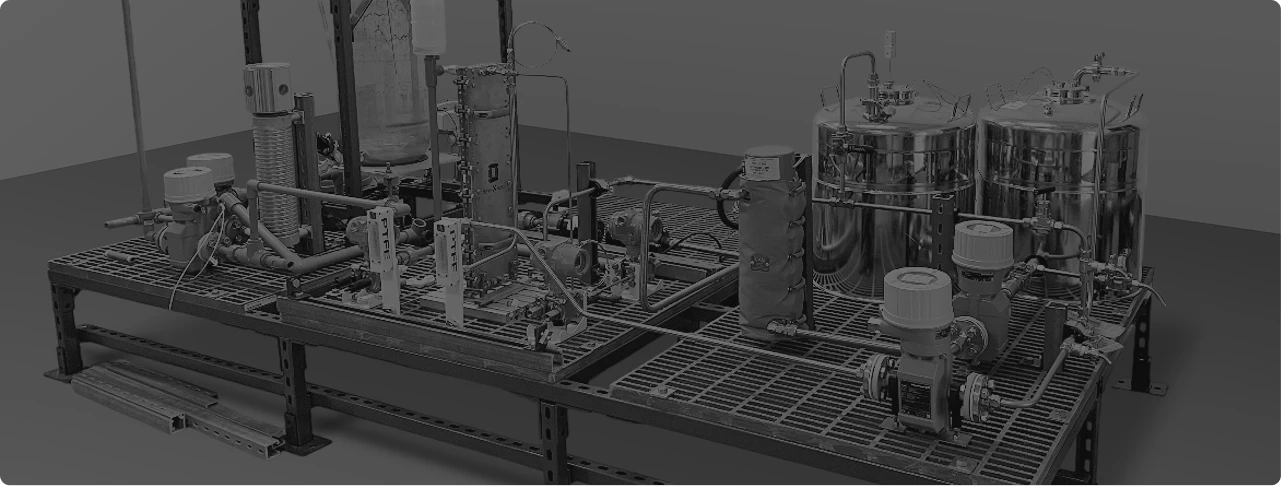

Onshoring of key supply chains is becoming increasingly important for the energy transition. To this end, the battery manufacturing supply chain outside of China is growing exponentially, but a major issue looms over the battery manufacturing process: waste. The production of one gigawatt-hour of batteries generates about 5,000 metric tons of a chemical byproduct called sodium sulfate. While Chinese battery companies can sell this byproduct into the Chinese detergent market, manufacturers based in the US and Europe are struggling to find offtakers for this material and instead must pay for its disposal. In the competitive battery industry, the difference between sodium sulfate being a sellable product and a cost center for disposal is one of the main reasons why battery producers in the US and Europe can’t compete on cost with Chinese battery companies.

In extreme examples, sodium sulfate waste can even lead to battery projects being delayed or cancelled. Recently, a BASF-owned battery cathode plant in Finland was denied an environmental permit to operate owing to the large quantities of sodium sulfate waste the plant would generate.

Demand for batteries, primarily driven by electric vehicles, is projected to grow at a 22% CAGR through 2030, with the global battery manufacturing supply chain projected to be a $400B market by 2030. Meeting net-zero targets will require battery manufacturing to increase ~5x by 2030. Project delays and cancellations exacerbate the supply-demand gap – a discrepancy we cannot afford if we aim to decarbonize major industries and achieve global climate goals by 2050. Put simply, sodium sulfate waste poses a colossal challenge for the battery supply chain and, resultingly, for progress towards our net-zero goals.